Income Subject To Tax Not Recorded On - Bad debt expense is limited to the specific charge-off amount 4000. Income subject to tax but not recorded on the books this year.

Pin On Test Bank For Intermediate Accounting 19th Edition By Earl K Stice James D Stice

Tax Bracket.

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Income subject to tax not recorded on. No deduction is allowed for any expenditure incurred in deriving such income. However like any general rule there are a myriad of exceptions including one excepting a limited partners share of ordinary income from a partnership. For tax purposes income is usually recognized by a corporation when payment is received while financial reporting.

To date there has never been a tax on investment income. Such income is not chargeable to tax under any head of income in computing the taxable income of the person. Expenses recorded on the books this year but not deducted on this return.

The IRS has released a Form 8960 in draft and this will be the form we use. Subsequent sale of non-listed shares in a domestic corporation by individuals and domestic corporations are now subject to 15 capital gains tax. We recorded deferred charges during the year ended December 31 20X1 related to the deferral of income tax expense on intercompany profits that resulted from the sale of our intellectual property rights including intellectual property acquired during the current year outside North and South America to.

The sales tax for the above transaction is. UBTI or Unrelated business taxable income or the income itself that is subject to taxation. However these are not wages subject to income tax withholding so the partner will have to report these payments as income on their tax return whereas the draws are not treated as income.

UDFI is Unrelated Debt-Financed Income or a UBIT tax applied to debt financing which is. This is not a common item on a partnership return particularly for any entity that operates on a Cash Basis for accounting and tax reporting. Tax Rate for Qualified Dividends Capital Gains 9950.

As you apparently received no monetary payments as income from what you say it would appear you did not receive a Form W-2. The tax issue is that although you had no taxable income relative to either Federal or State income tax the value of the Housing Allowance is subject to a tax which is the equivalent of Social Security FICA and. For income subject to tax not recorded on books this year corporations report income which is currently recognized for tax purposes but not for financial accounting.

Source dividend The amount of the such income is not reduced by Any deductible allowance. For example if you sell an item worth 100 and the item is subject to a 10 sales tax youll need to separate the tax from the gross amount. Dividend income of an individual citizen and a resident alien received from domestic corporations is subject to 10 final withholding tax.

Income subject to tax not recorded on the books. BIR Form No. Income Subject to Tax Not Reported on the Books - In this section the user will enter any income that was included on the tax return but not included on the books of the business.

If a partner receives guaranteed payments during the year their Schedule K-1 will report their guaranteed payments as a separate line item from any draws. On the other income item line income subject to tax not recorded on books this year corporations report income which is currently recognized for tax purposes but not for financial accounting. Income subject to tax not recorded on books.

Since the business is collecting sales tax on behalf of tax authorities the tax is not recorded as a part of the revenue. However for financial reporting the company is required to recog-. Deductions on the tax return but not charged against book income this year.

All fields are None 2. Income Not Recorded If a company has used some of its capital to invest in tax-exempt bonds or securities the income generated isnt required to be on the Schedule K of the tax return. And expenses recorded on the books not deducted on the return must be added to book income.

Income recorded on the books this year but not included on this return and. Expenses recorded on books this year not deducted on this tax return. This Certificate should be attached to the Annual Income Tax Return - BIR Form 1701 for individuals or BIR Form 1702 for non-individuals.

Dividends received by domestic and resident foreign corporations from another domestic corporation are exempt from income tax. Tax imposed is a final tax. Excess capital losses over capital gains.

Tax Rate on Regular Income. Federal income taxes. UBIT or Unrelated business income tax is the tax itself that is applied by the government on such taxable income.

2304 is a Certificate to be accomplished and issued by a Payor to recipients of income not subject to withholding tax. Beginning January 1 2013 most of us now realize that there will be a 38 net investment income tax on at least a portion of the gain when you have capital gains ordinary interest dividends and rental income. For tax purposes when a payment is received a company generally recognizes it as income.

Form 1120S Schedule M-1 Line 5 is where this type of income goes. There are no items of income subject to tax that are not already recorded on the corporations books. Income recorded on the books but not included on the return including tax-exempt interest and deductions on the return not charged against the books must be subtracted from book income.

Generally a taxpayers share of ordinary income reported on a Schedule K-1 from a partnership engaged in a trade or business is subject to the self-employment tax.

What Is Professional Tax Legal Services Tax Tax Accountant

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition Calculation

Accounts That Can Be Adjusted Accrued Revenues Accrued Expenses Deferred Expenses And Deferred Revenues Accounting Principles Accounting Fixed Asset

Deferred Tax Asset Definition Calculation

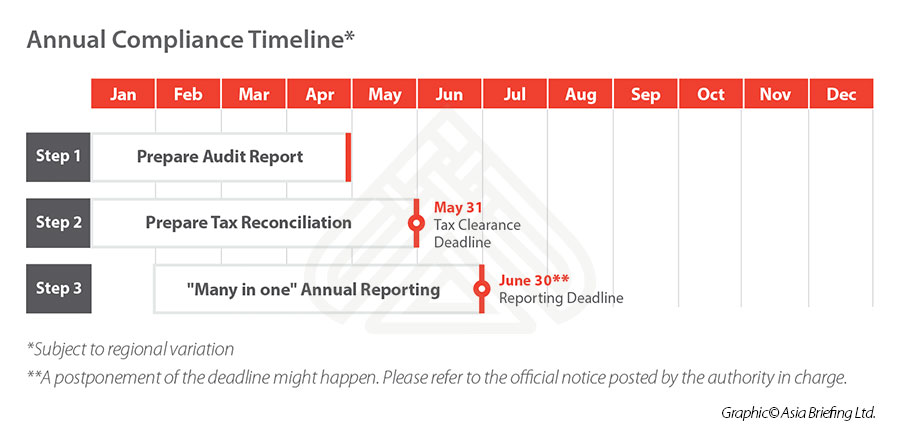

Preparing For Annual Tax Reconciliation In China In 2021 Faqs

:max_bytes(150000):strip_icc()/AppleIncomeSattementDec2019-cd967d0a8f5e4748a1060f83a7e7acbc.jpg)

Net Income After Taxes Niat

Income Tax Definition And Examples Market Business News

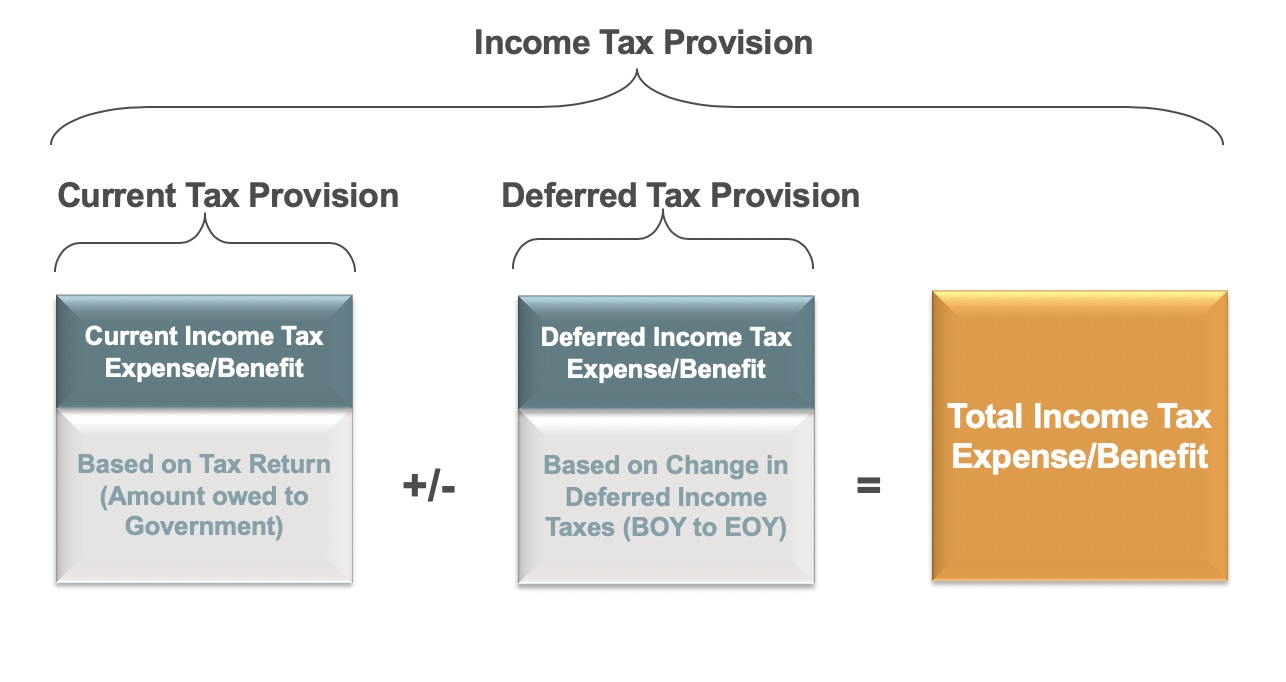

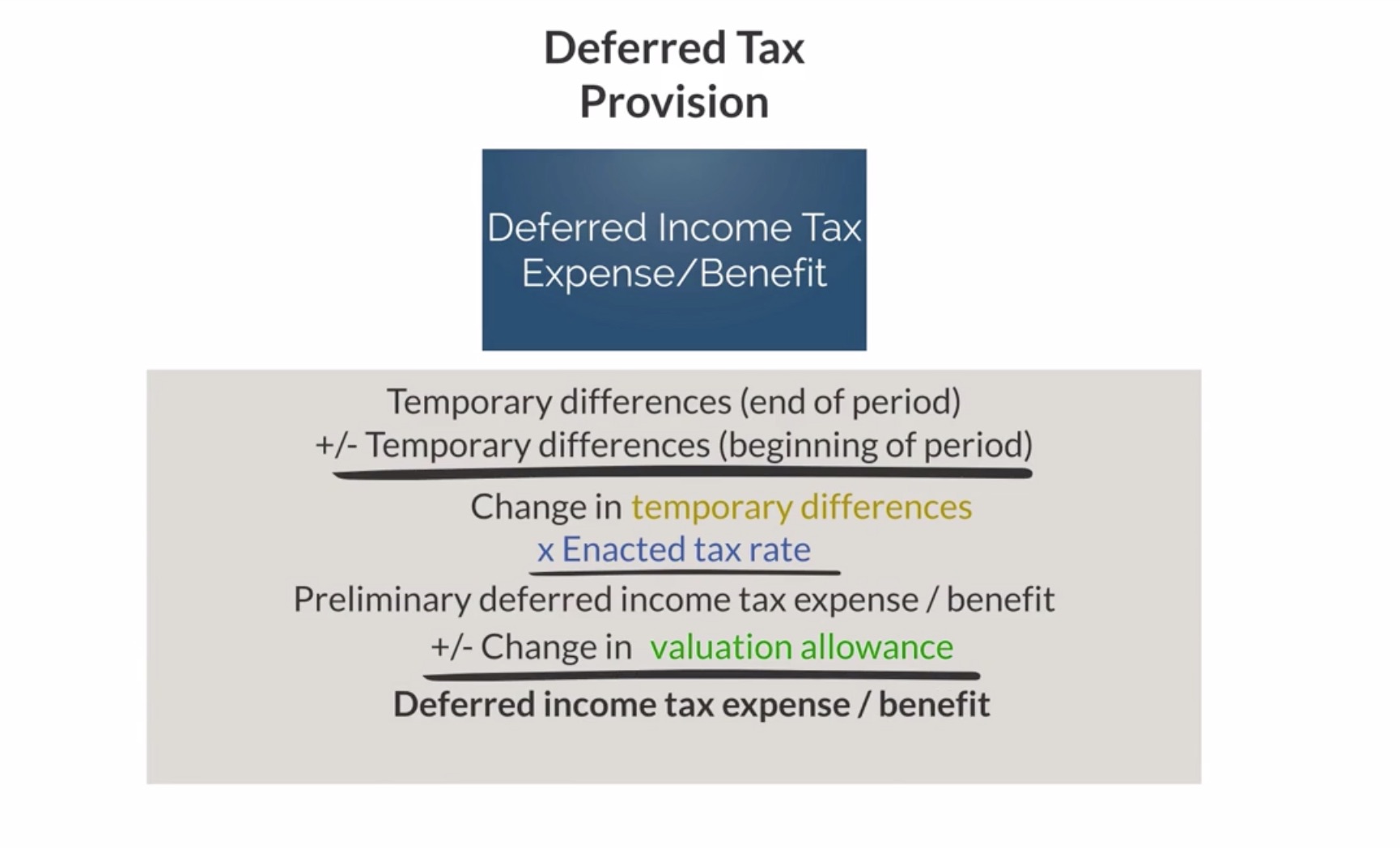

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

Tax Exemption Steps For Getting An 80g Certificate Tax Accounting Books Tax Exemption Tax

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

1120 Calculating Book Income Schedule M 1 And M 3 K1 M1 M3

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition Calculation

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

Pin On Test Bank For Intermediate Accounting 19th Edition By Earl K Stice James D Stice